Gross Pay vs Net Pay: What's the Difference?

You got a job offer for $55,000. You're excited. You start planning your budget around that number.

Then your first paycheck arrives and it's nowhere near what you expected.

That's the gross vs net pay gap — and almost everyone hits it for the first time without warning.

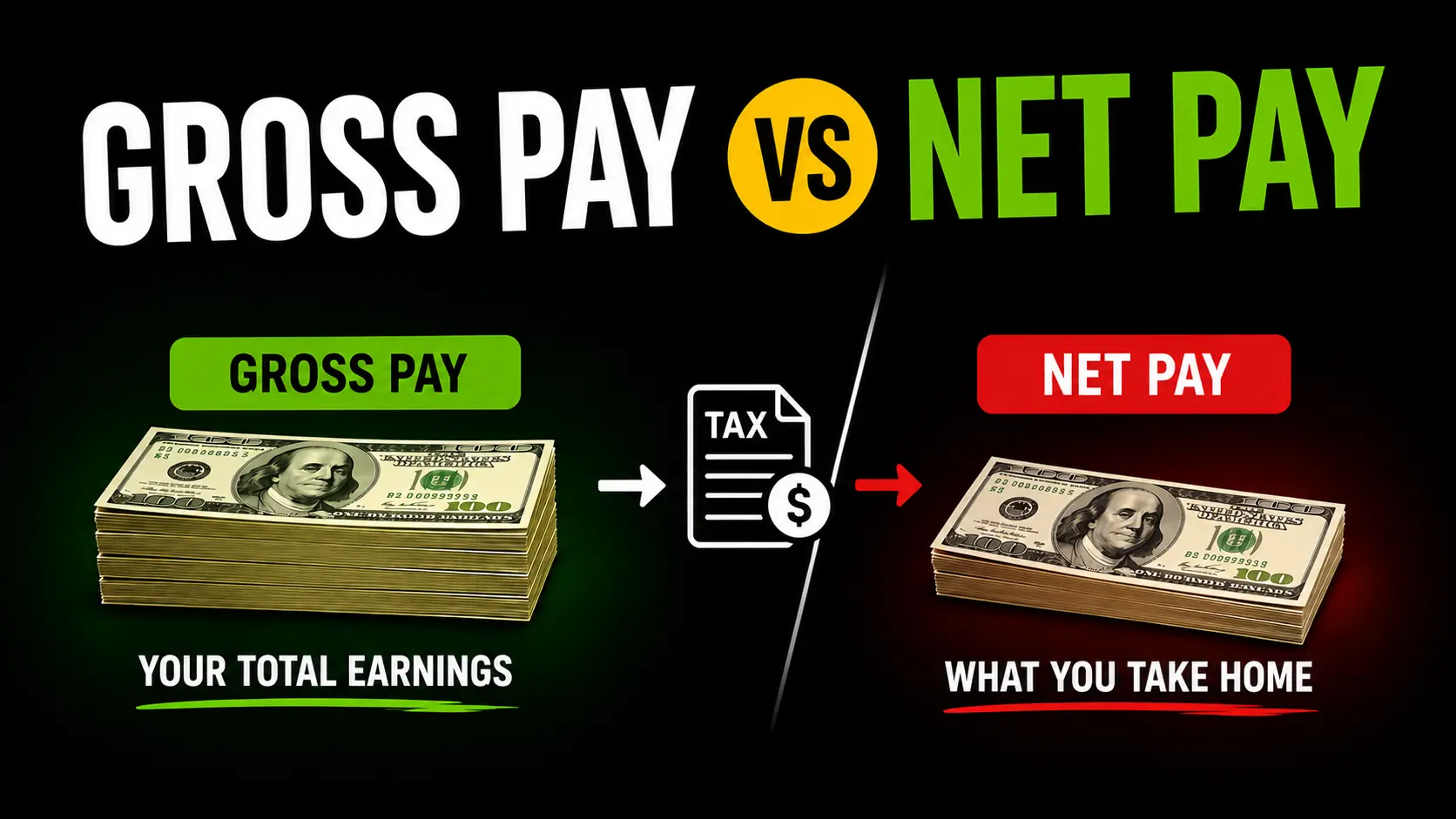

What is Gross Pay?

Gross pay is what you earn before anything is taken out. It's your full salary, your hourly rate times hours worked, any overtime, any bonuses — all of it, before taxes touch a cent of it.

It's the number employers use when they talk about compensation. "We're offering $55,000 a year." That's gross. It's also what shows up at the top of your pay stub, usually labeled "gross earnings" or "gross pay."

Think of it as the starting line. Everything that happens next reduces it.

What is Net Pay?

Net pay is what's left after all the deductions are done. Taxes, Social Security, Medicare, health insurance, retirement contributions — whatever applies to you gets subtracted from gross, and the number remaining is your net pay.

It's also called take-home pay. Because it's literally what you take home.

For most Americans, net pay is somewhere between 65% and 80% of gross pay. The rest goes to taxes and deductions. On a $55,000 salary in a no-state-tax state, you're realistically taking home around $43,000–$45,000 a year. In California or New York, closer to $38,000–$40,000.

What Turns Gross Into Net

A few things are mandatory — you don't get to opt out of these:

Federal income tax — based on your income level and filing status. The US uses a progressive system, so the more you earn, the higher the rate on the top portion. On $55,000 as a single filer, your effective federal rate ends up around 11-12%.

Social Security — 6.2% flat, every paycheck, up to the 2026 wage base of $184,500.

Medicare — 1.45% flat, no cap, every paycheck.

State income tax — depends entirely on where you live. Texas, Florida, Nevada, Washington — zero. California, New York, New Jersey — significant. Nine states have no income tax at all.

Then there are the voluntary deductions — things you signed up for that also come out before you see the money:

Health insurance premiums, if your employer shares the cost with you. 401(k) contributions, if you're saving for retirement through work. HSA or FSA contributions, dental, vision — anything you elected during benefits enrollment.

These voluntary deductions are why two people earning the exact same gross salary can have completely different paychecks. Same $55,000. One is contributing 10% to a 401(k) and has the premium health plan. The other has basic coverage and no retirement contributions. Their net pay can differ by $400-$600 per month.

Side by Side

Here's what it looks like on a real paycheck. Single filer, $55,000 salary, Texas, biweekly pay, no voluntary deductions:

Gross per paycheck: $2,115

Federal income tax: −$237

Social Security: −$131

Medicare: −$31

Net pay: ~$1,716

That's $399 less per paycheck than gross — $10,374 less per year — just from mandatory federal taxes. Before health insurance or retirement savings even enter the picture.

Want your exact number? The paycheck calculator handles federal tax, FICA, and state tax so you don't have to do this manually.

Why This Actually Matters

Beyond just understanding your paycheck, knowing the gross vs net difference matters in a few practical ways.

When you're budgeting, you budget from net — not gross. A lot of people make the mistake of planning their expenses around their salary number and then wondering why things feel tight. Build your budget around what actually hits your account.

When you're negotiating salary, employers talk in gross. So when you're comparing offers or asking for a raise, you're comparing gross numbers — which is fine, just remember to mentally convert both to net before deciding which one actually puts more money in your pocket. A higher salary in California can net less than a lower salary in Texas.

When you're evaluating benefits, the value of employer-provided health insurance is essentially the difference between what you'd pay for it on your own vs what comes out of your paycheck. That gap is part of your total compensation, even though it doesn't show up in your net pay.