How Much Will My Raise Be After Taxes?

You just got a raise. Maybe it's 5%, maybe it's a flat $5,000, maybe it's a promotion bump. Either way, the number your manager told you isn't the number that hits your bank account.

Taxes take a cut first. And depending on your salary and where you live, that cut can be surprisingly large.

Here's exactly how it works — and what you'll actually keep.

Short Answer

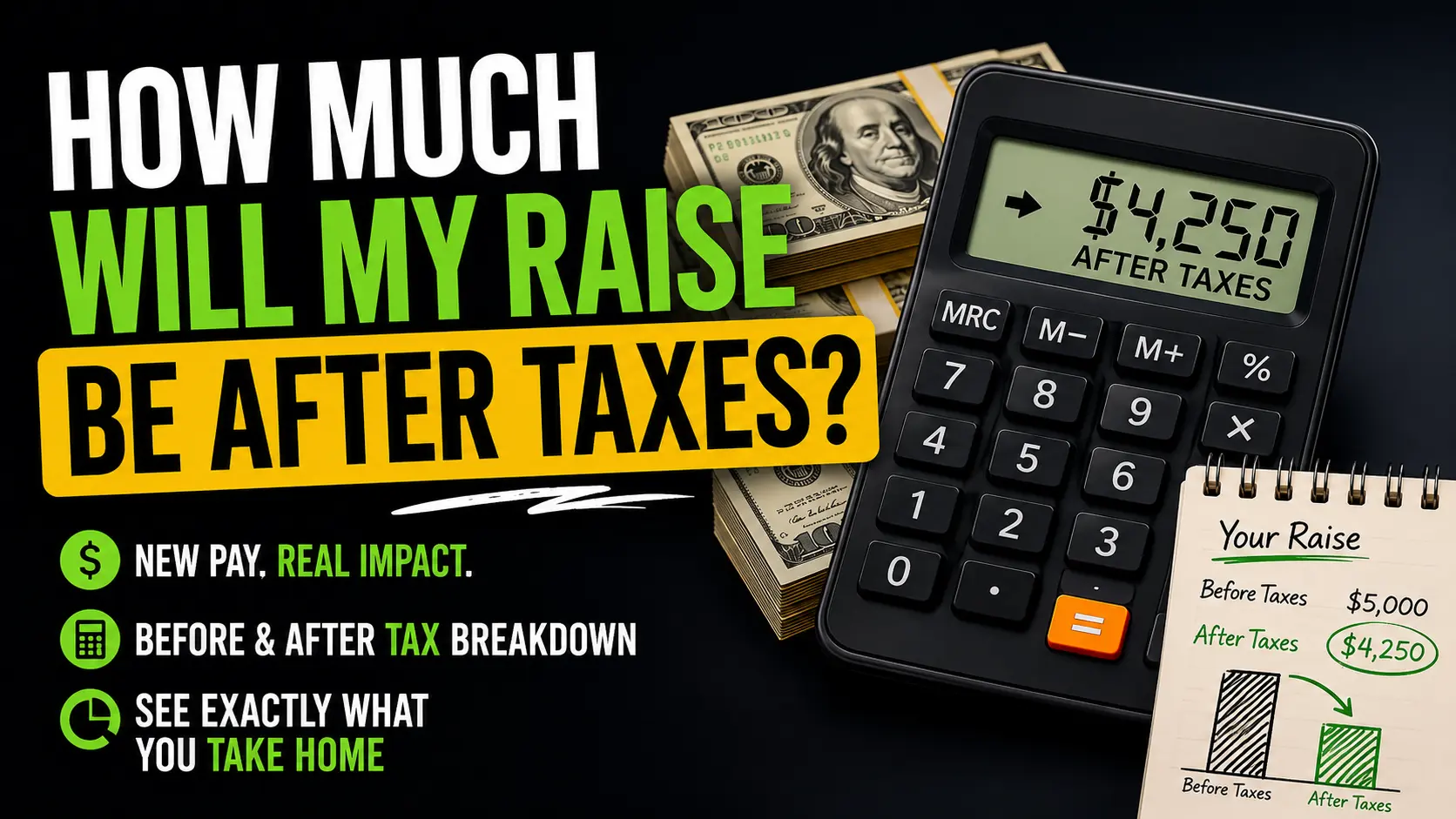

For most Americans, you keep roughly 65 to 75 cents of every extra dollar from a raise. The rest goes to federal income tax and FICA (Social Security and Medicare). State income tax takes even more if you're in a high-tax state like California or New York.

That means a $5,000 raise typically adds somewhere between $3,250 and $3,750 to your annual take-home pay — not $5,000.

Why You Don't Keep the Full Amount

When you get a raise, that extra income gets taxed at your marginal rate — the rate that applies to the top slice of your income, not your whole salary.

If you're in the 22% federal bracket, every extra dollar from your raise loses 22 cents to federal income tax right away. On top of that, Social Security takes 6.2% and Medicare takes 1.45%. That's already 29.65% gone before state taxes even enter the picture.

So no, a raise doesn't feel as big as it looks on paper. That's not a bug in the system — it's just how marginal taxation works.

Let's Understand With an Example

Here's what a $5,000 raise looks like after federal taxes and FICA across a few common salary levels, filing as single:

$45,000 salary (12% federal bracket)

Federal tax on raise: ~$600

FICA on raise: ~$383

Extra take-home: ~$4,017 per year / $154 per biweekly paycheck

$70,000 salary (22% federal bracket)

Federal tax on raise: ~$1,100

FICA on raise: ~$383

Extra take-home: ~$3,517 per year / $135 per biweekly paycheck

$110,000 salary (24% federal bracket)

Federal tax on raise: ~$1,200

FICA on raise: ~$383

Extra take-home: ~$3,417 per year / $131 per biweekly paycheck

The higher your salary, the more of your raise goes to taxes. But you always come out ahead — a raise never makes your take-home go down.

What About State Taxes?

If you live in Texas, Florida, Nevada, or Washington, you pay zero state income tax on wages. Your numbers above are your real numbers.

In California, add roughly 9.3% state tax on that extra income at the $70k level — which drops your extra take-home closer to $2,800 on a $5,000 raise. New York takes a similar bite.

State taxes can make a meaningful difference, especially for larger raises. That's why two people with identical salaries in different states can end up with noticeably different take-home pay.

Does a Raise Push You Into a Higher Tax Bracket?

It might — but it doesn't work the way most people fear.

The US tax system is marginal, which means only the income above a bracket threshold gets taxed at the higher rate. Not your entire salary.

If your raise pushes $2,000 of income from the 22% bracket into the 24% bracket, only those $2,000 get taxed at 24%. The rest of your raise still gets taxed at 22%. Your total paycheck doesn't shrink — it just grows a bit less than it might have otherwise.

The myth that a raise can "cost you money" by bumping your bracket is exactly that — a myth.

How to Calculate Your Raise After Taxes

The quickest way is to use our pay raise calculator — enter your current salary, your raise amount or percentage, and your filing status. It shows your new salary, the extra take-home per year, per month, and per biweekly paycheck, plus a full before-and-after tax breakdown.

If you want to do it manually, here's the process:

Step 1: Find your federal marginal rate based on your taxable income (gross minus standard deduction).

Step 2: Multiply your raise amount by that rate to get federal tax on the raise.

Step 3: Multiply your raise by 7.65% for FICA (6.2% SS + 1.45% Medicare).

Step 4: Add your state marginal rate if applicable.

Step 5: Subtract all of that from your raise amount. What's left is your actual take-home increase.

It's doable but tedious, especially with state taxes in the mix. The calculator handles all of it in seconds.

Raise vs Bonus: Which Puts More in Your Pocket?

This comes up a lot. A $5,000 raise and a $5,000 bonus are not the same thing financially — even before taxes.

A raise permanently increases your base salary. That compounds with future raises, affects your 401(k) match if it's percentage-based, and raises your baseline for any future negotiations. A bonus is a one-time payment that doesn't change your salary going forward.

Tax-wise, bonuses are often withheld at the 22% supplemental federal rate regardless of your actual bracket, which can mean over-withholding if you're in a lower bracket. A raise is withheld at your normal rate spread across paychecks.

Over a 5-year career, a $3,000 raise almost always outperforms a $3,000 bonus in total financial impact — even if the immediate dollar amount looks identical.